Purchasing a condo is an exciting milestone event. Many first-time homebuyers choose to invest in a condominium because it is more affordable than a detached home, but there are plenty of other good reasons to move into a condo community. Below, we’ll look at how sale prices and down payments vary depending on where you live.

Buying a house vs. buying a condo

The pros of purchasing a condo are that you get to enjoy a wide range of amenities, which may include a gym, door service and security, shared outdoor space, a party room and a pool. As a condo owner, there are also fewer things you have to maintain. For example, you don’t have to worry about repairing the roof or mowing the lawn. The corporation or association is responsible for scheduling repairs and maintaining the property. Of course, these services come at a cost. All condo owners must pay condo fees which are used to keep the building in good condition.

Convenience is another selling point. Condos are usually constructed within walking distance of offices, schools, grocery stores, restaurants etc. People don’t need cars to get around, and they spend less of their free time commuting. Owners generally have easy access to public transportation, too. They’re closer to more people, which means there are more opportunities for social interactions.

Now for the financial considerations. If you need a mortgage to buy a condo, it helps to understand how condo financing works. While condos are generally more affordable than single-family homes, buying a condo with a mortgage can sometimes be surprisingly difficult.

With standalone houses, a bank appraises the home and checks to make sure there is a clean title before approving a buyer for a mortgage. But when assessing a condo, the bank may also consider the finances of the association/corporation. Banks want to see condo documents and ensure there aren’t any problems that would bring down the property’s value. Moreover, they may investigate how many rental units and vacant units are in the condo development. It would use this information to determine how well the property will hold its value.

Average price for a down payment

No matter what type of home you are buying, the more you can pay upfront, the better. Lenders feel more comfortable giving mortgages to owners who can cover a larger portion of the sale price on their own. That’s because they are more likely to get all of their money back if the owners happen to default on their loan. The smaller the risk, the less they charge in mortgage insurance. It is also easier to make fewer payments when there is less debt owed, which means you spend less of your money in the long run.

Buyers are encouraged to put 20% down because they will be eligible to receive an uninsured mortgage. But many buyers simply don’t have that kind of money, especially in states or provinces where the average sale price is above $500,000. Below, you’ll get a better idea of what an average down payment for a condo looks like in a few different places.

Toronto

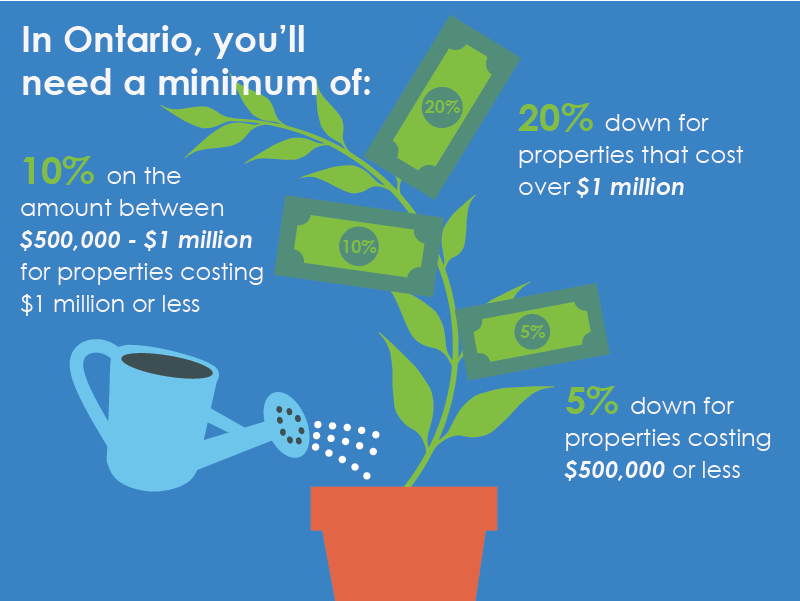

In Canada, most mortgage regulations are set by the federal government, so rules are very similar in all provinces and territories. Mortgage default insurance, also referred to as CMHC insurance, must be purchased on all mortgages with down payments of less than 20%. However, this insurance is not available for homes costing $1 million or more.

When buying a condo in Toronto, owners can put down 5% of the total purchase price of a condo costing less than $500,000. For condos that cost $500,000 to $999,999, owners must pay 5% of the initial $500,000 of the total purchase price, and 10% of the remaining price above $500,000. For condos costing $1 million and above, owners must pay 20% of the total purchase price of the condo. This is true for other provinces and territories in Canada as well.

Note that if you are self-employed or have a poor credit score, the down payment amount required for your condo might be higher than the minimum requirement.

In 2021, the average sale price of a condo in Toronto is roughly $720,000. The market remains hot, and all types of homes are expensive. That means owners would be looking at a down payment of $47,000.

Edmonton

Unlike many other Canadian provinces, Alberta does not charge a land transfer tax on property purchases. Instead, a land title transfer fee is charged. This is generally more affordable than a land transfer tax, making Alberta a relatively affordable place to invest in a condo.

The average condo sale price is about $241,808 in Edmonton. So, that means buyers only need to put 5% down. The down payment cost would amount to $12,090.

Chicago

In the United States, some believe that they must put down 20%, but this is not true. While there are obvious advantages to making such a large payment, owners can pay as little as 3% depending on the type of loan and the lender’s criteria.

FHA loans, for example, require a minimum of 3.5% down. But, applicants must have a minimum FICO score of 580 to qualify. If the buyer’s credit score is below 580, the down payment requirement is 10%.

According to a 2020 survey conducted by the National Association of Realtors, first-time homebuyers who financed the purchase made a median down payment of 7%. The median down payment for repeat buyers who financed was 16%. For simplicity’s sake, we will use the 7% marker to help us calculate average down payments in different states.

The average sale price of a condo in Chicago was listed at approximately $365,000. A 7% down payment would come to $25,550.

Florida

Sale prices for Florida condos sit at about $272,000. Real estate prices continue to climb here thanks to the state’s low taxes, warmer weather, and thriving economy. The average down payment for a condo in Florida would be roughly $19,040.

California

Housing is much more expensive in this state. The average sale price of a condo is about $655,000, making the average down payment $45,850.

Tips to help you save for a down payment

Saving thousands of dollars for a down payment can be challenging. Experts recommend these strategies to make the process a bit easier.

- Set up monthly goals for saving, and track the amount that makes it into your down payment fund. Goals need to be specific and realistic in order to be attainable

- Consult with multiple lenders. Although it takes more work, speaking to different lenders could save you thousands of dollars. Some statistics show that getting the right financing for your individual situation can save you $9,000 over the span of a 30-year mortgage

- If you have credit card debt, work on getting rid of that first. Interest rates are high, which makes this a costly debt to carry around. Once it’s gone, you can put that extra money towards your down payment

- Save bonuses, tax refunds and raises instead of making a lavish purchase

Conclusion

Buying a condo is a joyous occasion, but it is also a serious financial investment. Buyers who have a concrete understanding of what they can afford, and when they should buy, will be in a good position to make the best choice for their unique situation.