As an HOA board, financial management sits at the heart of everything you do. And I’m not just talking about collecting assessments. I mean the full picture, from building accurate budgets, maintaining a healthy reserve fund, to producing timely financial statements, and keeping yourself accountable to the homeowners who elected you. When this breaks down, you end up with special assessments, strained cash flow, and damaged board credibility.

And remember, you are volunteers. In fact, you probably already spend somewhere between 6 and 10 hours a month on board responsibilities such as meetings, prep, and emails. At the same time, you have careers, families, and lives outside the community. The result is burnout, which is already a growing threat to effective governance. But the truth is that this burnout often traces back to operational tools that weren’t designed for this work.

With the financial management burden in mind, one of the most important tools in your hands is the payment tool. If this tool works right, it should reduce manual errors, eliminate lost checks and open invoices, and take the most tedious financial tasks completely off your plate. But the truth is not every platform is designed with HOA life in mind, and picking the wrong one just means you’ve digitized the same problems you already had.

So what should you actually be looking for? In my experience working with community associations, there are 3 features HOA boards want most in a payment tool. Let me walk you through each one.

Accounting integration

HOA accounting runs on a rhythm. Every month, the same cycle repeats: generate assessment invoices, process incoming payments, record transactions, reconcile bank accounts, and prepare financial statements.

Bank reconciliation alone should happen at a minimum once a month. It’s how you’ll catch uncashed checks, duplicate payments, and auto-drafts that slipped through unrecorded. But when your payment tool doesn’t connect directly to your accounting system, every single one of those steps becomes a manual handoff, and every handoff is a point of failure.

The cost of disconnected systems

A surprising number of associations are still managing their books through general-purpose tools like QuickBooks and Excel spreadsheets. These tools look familiar, they’re accessible, and they feel manageable at first. But QuickBooks wasn’t built for HOA accounting. The workarounds pile up fast, and double data entry becomes routine. Then reporting turns into a project instead of a process.

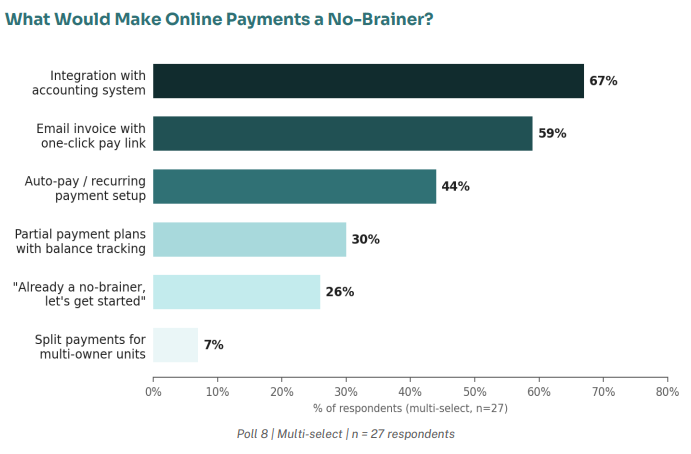

We hosted a webinar with 27 HOA leaders, and QuickBooks frustrations were the single hottest topic in the Q&A, generating five separate questions from attendees trying to figure out how to work around its limitations. That sentiment was reflected directly in our webinar findings: 67% of the HOA leaders polled ranked accounting system integration as a deciding factor when evaluating a payment tool, making it the most demanded feature of all three covered in this guide. In fact, according to CAI, accounting issues rank among the top three complaints boards raise about legacy software.

Let me show you why accounting integration indeed is a viable deciding factor. A $50 discrepancy today becomes a $500 mystery six months later when no one can reconstruct the original transactions. When boards build complex workarounds to make a general accounting tool function for HOA purposes, those workarounds live in the treasurer’s head – and when that treasurer rotates off the board, so does the institutional knowledge. The next person inherits a system they can’t decipher, and financial continuity takes the hit.

What the data says about manual entry

According to the Journal of Accountancy, human error rates in manual data entry range from 1% to 5%, depending on complexity. Out of 10,000 entries, automated systems produce 1 to 4 errors. On the other hand, humans produce between 100 and 400. Poor data costs organizations about $12.9 million annually. Roughly a third of accountants admit to making data entry mistakes multiple times a week, and finance teams using automated reconciliation tools report a 95% reduction in errors compared to manual methods.

Although this data is from general accounting professionals, the math still applies to HOAs that manually enter payment data across payment tools and accounting systems. And because your HOA treasurer is likely a volunteer with no formal bookkeeping background, those odds are not in your community’s favor.

What integration looks like

True accounting integration means your payment data flows directly into your books without exports, copy-paste, and manual reconciliation. When a homeowner pays their assessment, that transaction is automatically processed. Bank feeds pull transaction data in real time. Your financial records stay current without anyone having to touch them.

The downstream effect on reporting is that you can pull balance sheets, income statements, and budget-versus-actual comparisons without waiting for the treasurer to compile everything from scratch. Real-time visibility means faster, better-informed decisions, and a board that can actually see where the money stands instead of guessing.

One-click email invoices

When collecting fees manually, someone has to generate the invoices. Someone has to send them. Someone has to track who’s paid and who hasn’t. Someone has to follow up by email, by phone, sometimes in person, with the neighbors who’ve gone quiet. And then someone has to match every payment to the right homeowner and the right ledger account before the month closes. That someone is you, a volunteer who signed up to help govern a community, not to run a collections operation.

There’s a well-established principle in consumer behavior that applies directly to dues collection: friction kills follow-through. Friction is anything that stands between a ready-to-pay person and completing that payment – an extra step, a confusing process, a moment of “I’ll come back to this later.” And we know from e-commerce research that even small improvements to the payment experience drive meaningful results. The Baymard Institute found that optimizing checkout design alone can improve conversion rates by as much as 35% on large platforms.

The HOA context isn’t different in any meaningful way. Homeowners aren’t refusing to pay because they don’t want to. Most of them just need the path to payment to be easy enough that they don’t procrastinate. Every extra click, every login step, every moment of friction nudges them one step closer to setting it aside. A single embedded pay link in an email they’re already reading removes almost all of that resistance.

What one-click email invoices mean for the board

In our webinar, 59% of the HOA leaders said email invoices with an embedded one-click pay link were among the features they wanted most in a payment tool. That’s not a small number. And it tells you something important: boards aren’t just looking for automation in the abstract, but they’re looking for the kind of frictionless experience that actually shifts homeowner behavior.

Instead of manually generating and sending invoices every cycle, the system handles the entire process for you. You configure the assessment amount, the billing frequency, and the due date. On the scheduled day, invoices go out automatically to every homeowner.

Then the follow-up runs on its own, too. Automated reminders go out before the due date, on the due date, and after, escalating as needed, and stopping the moment payment comes through. The system stays on schedule even when you’re traveling, busy with work, or simply not thinking about HOA finances. And because the reminders are automated rather than personal, they remove the social awkwardness of board members having to position themselves as collectors within their own community.

Auto-pay and recurring payments

When a homeowner falls behind on assessments, the easy assumption is that they’re unwilling to pay. But that’s usually not what’s happening. What’s far more common is financial hardship, a misunderstanding about what’s owed, a dispute, or something much simpler: they forgot. And data across industries proves this.

About 56% of Americans have missed a bill payment simply because it slipped their mind. That breaks down roughly evenly between people who overlooked the bill entirely and people who mixed up the due date. A separate LendingTree survey found that nearly 1 in 4 people who recently paid a bill late say they forgot it completely, and another 22% say they confused the due date.

That means in your community, a huge portion of your delinquency problem may have nothing to do with financial hardship, difficult homeowners, or disputes. It’s just a life of busy schedules, work pressure, travel, and family obligations – creating enough noise that a quarterly assessment slips through the cracks. That’s a very different problem, and it has a very straightforward solution.

Remove the need to remember at all

If forgetfulness is driving late payments, then the most effective intervention isn’t a better collection process, but eliminating the memory requirement entirely. That’s what auto-pay does. When assessments are automatically drafted from a bank account or charged to a card on a set schedule, there’s nothing for the homeowner to forget, no due date to track, and no payment portal to log into at the right moment.

Research from the National Bureau of Economic Research shows that autopay enrollment dramatically increases the probability of on-time payment and significantly reduces the likelihood of accounts sliding into serious delinquency. And in our webinar, 44% identified auto-pay and recurring payment setup as a priority feature. That’s a strong signal that boards aren’t treating this as a convenience add-on. They’ve come to see it as a core financial stability mechanism.

A few things to sort out before you launch it

Before rolling out auto-pay to your community, there are a couple of considerations worth getting right. First, check your governing documents. They’ll tell you whether your association is permitted to charge a processing fee for online payments, and if you do charge one, you’re obligated to disclose it clearly to homeowners and display it on the payment page itself.

On the platform side, auto-pay should always be opt-in. A homeowner enrolls when they’re ready, and they can opt out just as easily. Once they’re enrolled, the system handles the rest — communicating the amount due to the bank or card issuer and processing the payment to the association automatically when the invoice is generated.

What auto-pay delivers

The benefits of auto-pay run in both directions, and that’s worth emphasizing when you’re promoting enrollment to your community. For homeowners, it’s genuinely “set it and forget it” – no checks to write, no portals to remember, no late fees to dispute. For boards, it translates into something that makes every other aspect of financial management easier: predictable, consistent cash flow.

When you know what’s coming in each month, you can address maintenance issues faster, plan capital projects with more confidence, and operate without the constant anxiety of wondering whether assessments will cover the month’s obligations.

The key to unlocking those benefits is driving enrollment, and that takes a proactive approach. Promote auto-pay in welcome packets, on billing statements, in newsletters, and at annual meetings. A simple reminder a few days before an assessment cycle begins can be enough to prompt enrollment from homeowners who’ve been meaning to sign up.

Honorable mention: Partial payment plans

The three features above address the everyday rhythm of dues collection. But there’s one more capability worth talking about: special assessments. Special assessments range anywhere from $5,000 to $400,000, and with an estimated 70% of HOAs currently underfunded, the odds that your community will issue one at some point are genuinely high.

When a special assessment lands, the financial impact on individual homeowners can be severe. Most people simply cannot absorb a bill for $10,000, $20,000, or more within 30 days. For some, it creates real hardship. For others, it can push them into debt.

That’s why a payment tool that supports partial payment plans is a practical necessity. In our webinar poll of 27 HOA leaders, 30% specifically called out partial payment plans with balance tracking as a feature they wanted in a payment tool. Given what’s at stake when a large special assessment hits, that’s a significant share.

In many states, offering a payment plan isn’t optional

This is where boards sometimes get caught off guard. Payment plans aren’t just a goodwill gesture. In several states, there’s a legal requirement that must be offered before a board can escalate to collections or foreclosure.

For instance, in Colorado, HOAs must make a good-faith effort to work out an installment plan with a delinquent homeowner, covering equal payments over at least 18 months, before pursuing legal action. In Texas, associations with more than 14 lots are required to adopt formal payment plan guidelines so delinquent owners can make partial payments without accruing additional penalties.

In California, if a homeowner submits a written request for a payment plan, the board is legally obligated to consider it, and associations must disclose their payment plan policies as part of the annual statement sent to all homeowners. Skipping this step doesn’t just create legal exposure. It also eliminates your best opportunity to recover funds without the cost and conflict of formal escalation.

Where a payment tool makes this manageable

The traditional challenge with payment plans has always been the administrative overhead: tracking installments, applying payments in the right sequence, monitoring for defaults, and maintaining written agreements. For a volunteer board, that’s a lot of unpaid work.

A payment tool with built-in installment plan functionality changes. Homeowners can log into an online portal, review the board’s parameters, and set up their own payment arrangement without needing to schedule a call or sit across from a board member. The platform handles the structure: repayment term, payment frequency, interest rules, and late fee behavior, all configured in line with your governing documents and applicable state law.

Final thoughts

If you’re evaluating payment tools for your association, the place to start isn’t the feature list, but your own community’s pain points. Are late payments straining your cash flow? Is your treasurer drowning in manual reconciliation? Are homeowners complaining that paying dues is more complicated than it should be? Get clear on what you’re actually trying to solve, and then measure every platform you consider against those specific needs.

If we use the findings of our webinar as the measuring stick, the features that matter most are accounting integration, automated email invoicing with embedded pay links, auto-pay enrollment, and flexible payment plan support. When payment data flows directly into your books, when invoices go out and get paid without anyone chasing them, when auto-pay keeps dues current on enrolled accounts, and when payment plans give struggling homeowners a realistic path forward, you get better records, better cash flow, and no burnout.