As a board of a self-managed HOA, collecting monthly assessments is one of your primary responsibilities. Those dues fund everything, from landscaping and snow removal to building repairs and funding reserve funds. For years, the process has been straightforward: residents mail in checks, someone from the board picks them up, deposits them at the bank, and records the payment.

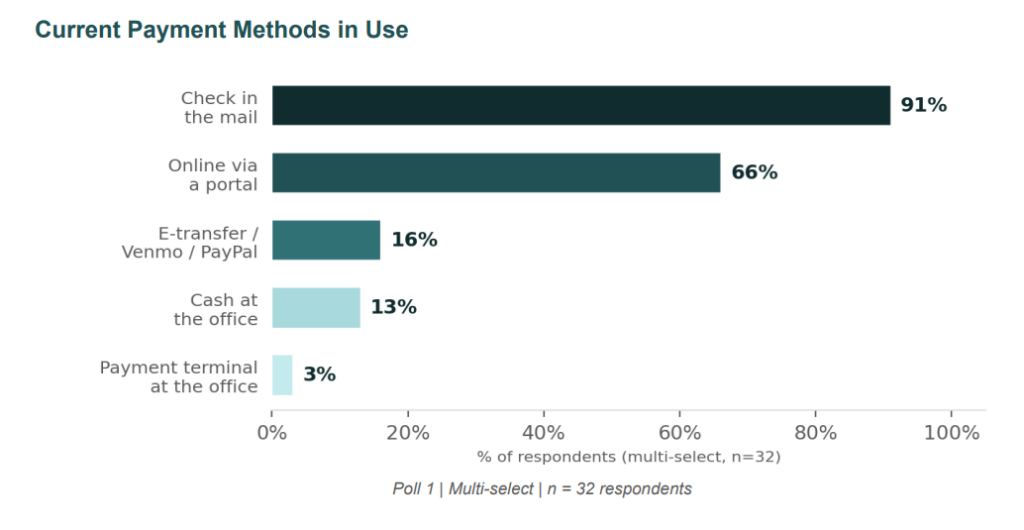

The process feels familiar, controllable, and safe, and probably that’s why most HOAs still hold on to it. In a recent study we did across HOAs, 91% of surveyed HOA communities still accept checks as a payment method. But familiarity isn’t the same as efficiency.

Paper checks have hidden costs, security risks, and operational issues that drain your association’s time and money. And just to make you see how inefficient checks have become, even federal agencies like the U.S. Treasury and Social Security Administration are actively working to eliminate paper checks in favor of electronic payments as part of a nationwide push toward safer, more efficient electronic transactions. If your board is still collecting checks as the primary payment method, here’s what it’s actually costing your HOA, and what you stand to gain by switching to online payment portals.

The real cost of collecting checks

Most boards think check collection is free or cheap because there’s no software subscription, no payment gateway, and no setup, but just an envelope and a trip to the bank. If you account for everything that goes into processing a single check, that picture changes. Here’s a breakdown of the hidden costs of check payments:

Labor and processing costs

Every check has to be logged, deposited, matched to the right unit, and reconciled in your records. Let’s assume that takes 10 minutes per payment. For an HOA with around 100 units, collecting all the checks and handling them will cost you 16+ hours. As a treasurer of a self-managed board, that time is coming directly out of your evenings and weekends.

Then there are the hard costs. The cost of processing a paper check is around $4 per transaction, when you throw in the labor, bank fees, and administrative costs that come with it. Electronic payments, by comparison, run about $0.28 per transaction. For a community processing even a few hundred payments a month, that’s thousands of dollars a year in unnecessary overhead.

Lost mail and delayed payments

Probably, you have been in a situation where a homeowner swears they mailed their dues check two weeks ago, but it still hasn’t arrived. You check the mailbox. Nothing. Now you’re both stuck. Do you charge a late fee? Do you ask them to reissue? Do you wait a little longer just in case it shows up?

Checks get lost, misdirected, or sit in a sorting facility for so long that the homeowner has to reissue another check. At the same time, vendors need to be paid, reserves need to be funded, and your ledger needs to balance, not forgetting you’ll still need to follow up with calls and updated records.

What makes this worse is the behavioral dynamic it creates. Once a homeowner drops a check in the mailbox, it mentally leaves their to-do list. They assume it’ll arrive. You assume it’s coming. And neither of you find out there’s a problem until it’s already caused one.

Check fraud

Check washing is one of the killers of check payments. According to the National Check Fraud Center, it costs Americans over $815 million every year. A criminal steals a check from a mailbox or a postal collection box, uses chemicals to erase the payee name and dollar amount, and rewrites the check to themselves for a much larger sum.

HOA and condo payments are prime targets of these fraudsters because they’re predictable. Criminals know that around the first of the month, mailboxes in residential communities will be full of checks made out for substantial amounts. That predictability makes your community a reliable hunting ground.

Once a check is washed and cashed, recovering those funds is a lengthy, frustrating process, and in the meantime, your association’s bank account has taken the hit.

Bounced checks

Then there’s the bounced check problem. A bounced check occurs when a bank returns a check unpaid due to insufficient funds, a closed account, or a signature issue. When that happens, the resident gets hit with a non-sufficient funds (NSF) fee, usually around $27 to $35 per check. In case of verification and signature issues, the bank places an extended hold on the deposit while it works through the verification process, sometimes 7 to 9 business days.

During that window, those funds appear in your account but aren’t actually available. If your board has already issued a vendor payment based on that apparent balance, you’re now looking at an overdraft situation on your end. That means fees on top of fees, and an accounting problem.

In the case of NSF, the ripple effect on the HOA includes returned check fees, delayed vendor payments, cash flow gaps, and the time spent chasing a replacement payment.

Late fees you can’t actually enforce

Late fees exist to protect the association’s cash flow, offset the costs your HOA incurs when assessments come in late, such as follow-up notices, time spent making phone calls, and penalties your association might face if you can’t pay your own vendors on time because cash flow is tight. Penalties also help signal to the community that dues collection is taken seriously.

The problem with check-based collection is that enforcing late fees fairly is virtually impossible. Let me give you an example. When a check doesn’t show up by the due date, what actually happened? Did the homeowner forget to mail it? Did it get delayed in transit? Is it sitting in a postal facility somewhere between their mailbox and yours? Was it intercepted? Did it arrive and get misplaced during processing? With a paper check, you can’t tell.

Now, what’s next? Will you charge the late fee? What if you then realize you’re penalizing a resident for a mail delay that was outside his control? Waive it, and you’ll have to explain why you didn’t penalize that homeowner, and you penalized another. Either way, you’re making a judgment call based on incomplete information, and those calls have a way of eroding trust over time.

Fair and transparent enforcement requires a clear paper trail. With check payments, that trail has gaps, and those gaps make it very difficult to apply your late fee policy consistently across the board.

The reconciliation nightmare

The next problem with checks: reconciliation. Every check that comes in has to be matched to the right unit, recorded in your accounting system, and verified against your bank statement.

When you’re manually entering check amounts, matching payments to units, and cross-referencing everything against bank statements, the opportunities for error are everywhere. Common errors include:

- Transposed numbers when entering a check amount

- A payment was logged to the wrong unit because two residents have similar names.

- A check that was deposited but never marked off in your records

- The same payment gets entered twice, inflating your cash balance on paper

- An outstanding check that never cleared is sitting in your books

- Timing differences, where checks take days to clear, can create discrepancies between what your records show and what the bank shows.

And the larger your community, the more likely something slips through. For example, in our study, we found a community with over 755 homes that relies entirely on manual check reconciliation. That translates to 755 checks a month, all being manually processed, matched, and entered. That’s a liability waiting to surface.

Why 66% of communities are running two systems at once

Checks haven’t stuck around because they’re better. They’ve stuck around because boards are trying to serve two different populations at the same time. On one side, you have younger homeowners, many of whom have never written a check. In fact, nearly 50% of Gen Z and millennials didn’t send a single check in all of 2023, according to GoBankingRates. For this group, mailing a paper payment feels as outdated as sending a fax.

On the other side, you have longer-tenured residents who are more comfortable with what they know. So what do most HOAs do? They try to accommodate everyone. They set up an online payment portal and keep accepting checks. In fact, in the recent study we did, we found that 66% of communities are running portals and checks simultaneously, with only 16% accepting electronic transfers like Venmo or PayPal.

It seems like a reasonable compromise, yes, but it’s worse than having checks alone. You’ll be dealing with two systems. Residents paying through your online portal have their payments automatically recorded, matched to the right account, and reflected in your financials in real time. Then a check arrives. Someone has to open it, log it manually, deposit it, and enter it into the system correctly for the books to stay accurate.

There’s also the enforcement problem I talked about. The online portal has clear records and automatic timestamps that make enforcement automated. On the other hand, check-paying residents don’t get penalties as they have lots of excuses to get waivers. That means you’re applying your dues policy inconsistently based solely on how someone chooses to pay. That’s not fair to the community, and it’s not sustainable for your board.

What a full transition actually looks like

The reality is that checks are on their way out. The U.S. government is phasing them out. Businesses across every industry are following suit. And if your HOA wants to protect its finances, reduce administrative burden, and operate like any other modern non-profit organization, I suggest you fully transition to electronic payment.

The key is approaching it without alienating anyone, including the residents who are still most comfortable with traditional methods. And here’s how to make that transition:

Start with the numbers

Before you can move your community toward electronic payments, you’ll likely need to go through the proper governance process, such as reviewing your CC&Rs and bylaws, getting homeowners involved, and, in many cases, putting it to a vote. And as any board member knows, getting a quorum or passing policy changes is the hardest part of HOA governance.

The most effective thing you can do to build support is to show your community their own numbers. When a homeowner sees exactly what their association is spending every month to collect and process paper payments, money that comes directly from their wallets, they’ll support a change.

Walk them through it. Take the number of checks your community processes in a month and build the real cost from the ground up:

- Supply costs of checkbooks, envelopes, stamps, and printer cartridges if checks are being printed on-site

- Mailing costs, including postage and any courier fees

- Labor costs consisting of the hours spent opening, logging, depositing, and reconciling each check, even if that’s a volunteer board member’s time

- Error and penalty costs such as late fees paid to vendors because a check arrived late, stop payment fees, returned check charges, and the time spent resolving disputes.

Add it all up, then place it next to the per-transaction cost of electronic payments. When residents see that their dues are subsidizing an inefficient system, they’ll support a change.

Address their security concerns

Some people hear “ online payment” and start thinking about hackers, data breaches, and fraud. The truth is that no payment system is completely fraud-proof. The question is which method gives you more control over your exposure and a faster path to recovery if something does go wrong.

With a paper check, once it leaves the mailbox, you have virtually no visibility into what happens to it. If it’s intercepted and washed, you may not find out for days or weeks after the damage is already done.

With electronic payments, you have real-time transaction records, automatic confirmation, and multiple layers of security built into the system, and on top of that, residents can protect themselves further with simple habits like strong passwords and not sharing logins. These are the same precautions people take with online banking, so nothing new for most people.

The goal isn’t to tell homeowners that digital payments are risk-free. It’s to help them understand that the risks are more visible, more manageable, and less severe than the risks they’re already accepting every time they drop a check in the mail. That reframing from “digital feels risky” to “paper checks are already risky and you just don’t see it” is the turning point for a lot of residents.

Choose a software built for HOA management

A general-purpose payment processor can handle transactions, but won’t automatically post a payment to the correct ledger category and won’t flag an outstanding balance against the right record. With such a platform, you’ll end up doing that work yourself, which defeats the purpose of automating in the first place.

When evaluating software for HOA management, look for something purpose-built for community association management. The right system should:

- Integrate with your existing accounting software so payment data flows in without manual re-entry

- Support multiple payment methods such as ACH, credit card, and eChecks, so you’re not forcing a single option on residents.

- Include security features like encryption and fraud detection that protect both the association and individual homeowners.

- Be intuitive enough that residents can navigate it without a tutorial, and board members can manage it without an IT background.

- Scale with your community as it grows and your needs evolve

Make the transition

Start by getting your platform configured and your homeowner data imported. Many modern HOA management systems can pull resident information directly from your existing accounting system records, which means the setup is far less painful. And if data needs manual entry, no worries, it’s a one-time task, and it’s done.

Then bring residents along gradually. For example, you can hold a short walkthrough through an email guide to show homeowners how to set up their account, link a payment method, and schedule their first payment. For residents who are less tech-comfortable, be available to answer questions during those first few months.

Final thoughts

Using the traditional paper check payments costs HOAs administrative time, money, stress, and introduces risks of fraud and reconciliation errors. Switching to online payment portals will address these issues because everything from payment collection, ledger entries, to reconciliation and financial reports generation is automated. And to realize the full benefits of automation, go for a platform designed specifically for HOA management. The platform will already know how to match payments to units, apply them to the right ledger accounts, reconcile your books, and generate industry-standard financial reports.